This post is also available in:

![]() Deutsch (German)

Deutsch (German) ![]() Español (Spanish)

Español (Spanish)

The petition is now open

You can sign the petition here now: https://epetitionen.bundestag.de/petitionen/_2026/_05/_30/Petition_201716.nc.html

How does the petition work?

The petition by the prohaltefrist.de initiative was submitted to the German Bundestag on May 30, 2026 (Petition 201716). It has been open for the public to sign since August 4, 2026. You can find the direct link at the top of this page.

Planned Process

1. Submission of the Petition

The petition was submitted on May 30, 2026.

2. Review by the Petitions Committee

After submission, the Petitions Committee of the German Bundestag reviews:

- whether the petition is admissible,

- whether it meets the formal requirements,

- and whether it will be published as a public ePetition.

As of August 4, 2026 – the review has been completed, and the petition has been made public and is available for viewing. It lasted from May 30 to August 4, which is significantly longer than the usual two to three weeks.

3. Public Co-Signing Phase

The official co-signing period has been open since August 4, 2026.

We have until:

September 15, 2026

to mobilize as many supporters as possible.

Why are 30,000 co-signers important?

If the threshold of:

30,000 co-signers

is reached within the co-signing period, the Petitions Committee may conduct a public hearing.

This gives the issue:

- significantly more political attention,

- public visibility,

- as well as official consideration in the German Bundestag.

Where is the petition signed?

The petition is co-signed exclusively through the official platform of the German Bundestag.

Once the petition has been published, we will post the direct link here on prohaltefrist.de as well as through our communication channels.

Petition Text

Title of the Petition

Preservation of the Tax-Exempt Holding Period for Private Disposal Transactions with Crypto Assets (Especially Bitcoin)

Text of the Petition

The petition calls for the preservation of the tax-exempt holding period for private disposal transactions with crypto assets (such as Bitcoin) under Section 23 of the German Income Tax Act (EStG). In particular, the one-year holding period, after which gains are tax-free, should not be abolished. Furthermore, it demands that the classification of crypto assets as “other economic goods” according to current administrative practice and case law be expressly maintained.

Justification (Summary)

The existing regulation ensures legal certainty for private investors, promotes long-term and responsible wealth building and personal retirement planning, and strengthens Germany as a location for innovation and business in the field of digital assets.

A change or abolition of the holding period or the current tax classification would lead to significant legal uncertainty, substantially hinder necessary private wealth building and personal retirement planning, and disadvantage Germany in international competition.

The necessity of this petition is based on essential procedural, economic, and bureaucratic arguments:

- Legal Certainty, Protection of Legitimate Expectations, and Private Retirement Planning

Citizens who have invested in crypto assets based on the current legal framework and established tax court case law rely on the dependability of the tax system. A retroactive elimination of the holding period would constitute a serious breach of the protection of legitimate expectations. Moreover, many small savers and private investors use Bitcoin and other crypto assets as instruments for long-term wealth building and private retirement planning. Those who hold digital assets for more than one year are not acting as short-term speculators, but as long-term investors. This form of personal retirement planning should be politically supported and not penalized through additional tax barriers.

- Securing Germany’s Competitiveness

The current tax exemption after twelve months makes Germany one of the most attractive and innovative locations for crypto investors and blockchain companies in Europe. Abolishing the holding period would represent a massive international competitive disadvantage. While countries like Switzerland leave crypto gains in private assets tax-free anyway and states like Portugal or the Czech Republic offer attractive holding periods, a tightening in Germany would drive capital, highly innovative Web3 companies, and skilled workers abroad.

- Reducing Bureaucracy and Relieving Tax Authorities

The existing one-year holding period functions not only as an investment incentive, but above all as a significant administrative simplification. If all transactions had to be declared regardless of holding period in the future, this would lead to immense documentation effort for millions of savers (e.g., through complex FIFO calculations across multiple wallets). Tax authorities would also face bureaucratic overload, as they would have to review countless micro-transactions and crypto reports, which would be disproportionate to actual tax revenues.

Maintaining the current practice thus protects citizens’ financial self-determination, prevents emigration, and avoids new, paralyzing administrative burdens.

As of May 30, 2026

How to Support the “Pro Holding Period” Petition

A Step-by-Step Guide to Co-Signing the Bundestag Petition

Many supporters ask us what data is required to sign a Bundestag petition and how the process works exactly.

That’s why we’ve created a detailed guide here.

The most important points upfront:

✅ Your address will not be publicly displayed.

✅ Your email address will not be published.

✅ You do not need to be a German citizen.

✅ You do not need to have a residence in Germany.

✅ After registration, you can also support all other Bundestag petitions in the future.

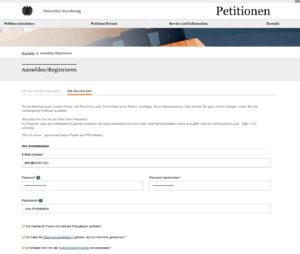

Step 1: Create a User Account with the German Bundestag

Before you can support a petition, you must create a free user account on the ePetition platform of the German Bundestag once.

👉 https://epetitionen.bundestag.de/epet/registrieren.html

Registration Form

The following information is required here:

- Email address

- self-chosen password

Additionally, you can provide a pseudonym.

Example:

Jens ProHaltefrist

The pseudonym is used voluntarily.

What is publicly displayed?

- Not your name.

- Not your email address.

- Not your address.

If you become active in the petition forum, only the chosen pseudonym will appear there.

If you do not enter a pseudonym, an anonymous identifier will be used automatically.

Consent to the Terms

Then three checkboxes must be checked:

☑ Privacy policy read

☑ Terms of use accepted

☑ Optional: Appear in the forum with pseudonym

Step 2: Provide Personal Information

In the next step, personal information is requested.

Required fields are:

- First name

- Last name

- Street and house number

- Postal code

- City

- Country

Optional:

- Title

- Organization

- Phone number

Must the information be genuine?

Yes.

The information must be plausible and truthful.

The German Bundestag requires this information to prevent multiple registrations and abuse.

Do I have to live in Germany?

No.

The petition can be supported by any natural person.

This includes, for example:

- German citizens

- EU citizens

- Persons from Austria

- Persons from Switzerland

- Persons with residence abroad

- Minors

The right to petition under Article 17 of the Basic Law expressly applies to:

“Everyone”

Step 3: Complete Registration

After all information has been provided, the platform confirms successful registration.

Now only one last step remains:

Confirming your email address.

Step 4: Confirm Email Address

Shortly after registration, you will receive an email from the German Bundestag.

Sender:

This email contains an activation link.

By clicking this link, you confirm:

- Your e-mail address

- Your user account

Step 5: Activate User Account

After successful activation, the confirmation appears:

“Thank you very much for registering. Your user account has been successfully activated and is now ready to use.”

This means that all requirements have been met.

Important: The petition has not yet been signed

Up to this point, you have only created a user account with the German Bundestag.

You can use this user account in the future for:

- the “Pro Holding Period” petition

- other Bundestag petitions

- discussions in the petition forum

use.

Step 6: Co-Sign the “Pro Holding Period” Petition

Once the petition has been published by the German Bundestag, we will post the direct link on this website.

Then you simply need to:

- Open the petition link

- Log in with your user account

- Click “Co-sign petition”

Your support will then be officially counted.

Frequently Asked Questions (FAQ)

Will my personal data be published?

No.

The following are generally not publicly visible:

- First name

- Last name

- Address

- Email address

- Phone number

Who can see my data?

The data is processed exclusively by the German Bundestag.

Only the responsible authorities have access within the framework of the petition process.

Can anyone tell that I own Bitcoin?

No.

With your signature, you are merely supporting the petition.

This does not reveal:

- whether you own Bitcoin,

- whether you own cryptocurrencies,

- or how much your assets are worth.

Do I have to be a German citizen?

No.

Any natural person can support the petition.

Do I have to live in Germany?

No.

Persons with residence abroad can also support the petition.

Can I provide false information?

We strongly advise against this.

The information must be truthful.

Obviously false or implausible information may result in the registration or co-signing being invalidated.

Will my email address be published?

No.

The email address is used exclusively for registration and verification of the user account.

Why does the Bundestag need my data at all?

The Bundestag wants to ensure that:

- each person co-signs only once,

- no automated mass registrations take place,

- and the co-signings actually come from real people.

Who is submitting the petition?

The petition is submitted by a group of dedicated individuals from the German Bitcoin and crypto community.

The official submitters are referred to in the parliamentary process as:

Petitioners

designated.

You can find all petitioners here: